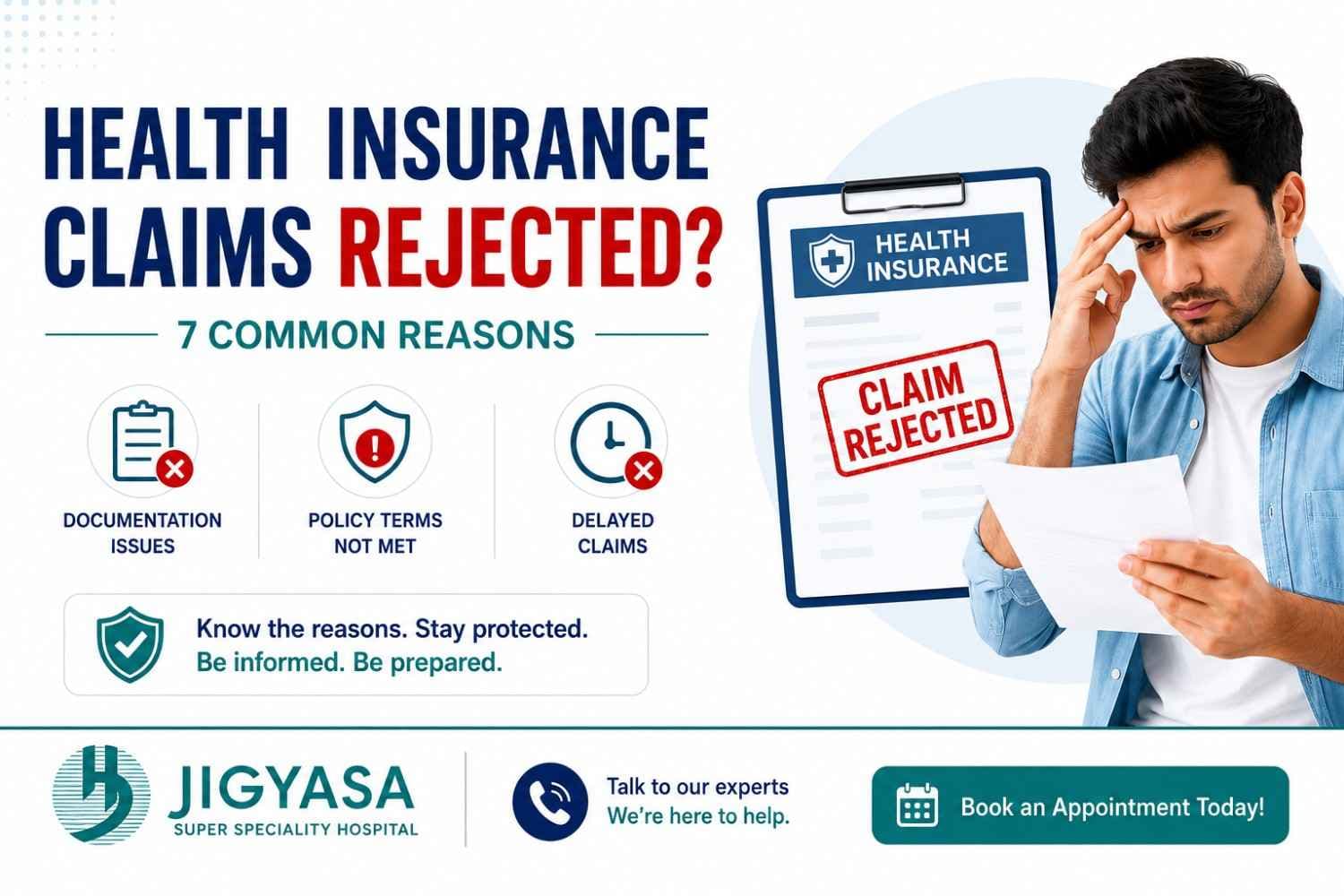

Health Insurance Claims Rejected? 7 Common Reasons

Getting Your Health Insurance Claim Rejected Is Stressful and Costly — Jigyasa Hospital Moradabad Explains the 7 Most Common Reasons Claims Get Denied and How to Avoid Them Before Your Next Hospitalisation

You faithfully paid your health insurance premiums for years, and then the moment you actually needed the coverage, your claim came back rejected. In India, health insurance claim rejections are more common than most policyholders realise — and the reasons are almost always preventable with the right knowledge. At Jigyasa Hospital, Moradabad, our patient support team assists hundreds of families every year in navigating insurance claims — cashless, reimbursement, and Ayushman Bharat (PM-JAY). This guide covers the 7 most common reasons health insurance claims get rejected in India, and exactly what you can do to protect yourself and your family.

Reason 1: Non-Disclosure of Pre-Existing Conditions

What happens: If you did not declare a pre-existing illness — like diabetes, hypertension, thyroid disorder, or heart disease — while buying your policy, the insurer can reject any claim related to that condition.

Why it's a problem: Insurance companies treat non-disclosure as a breach of the policy contract, giving them full legal right to deny your claim — even years later.

How to avoid it:

- •Always disclose every pre-existing medical condition honestly at the time of policy purchase.

- •Declare even conditions that seem minor — high cholesterol, obesity, past surgeries, or any ongoing medication.

- •Keep a copy of your filled proposal form for future reference.

Important: After the waiting period (typically 2–4 years depending on your policy), pre-existing conditions are covered — but only if they were disclosed upfront.

Reason 2: Treatment During the Waiting Period

What happens: Most health insurance policies include a waiting period — a defined duration after policy purchase during which certain treatments are not covered.

Types of waiting periods in India:

- •Initial waiting period (30–90 days): No claims allowed except for accidents.

- •Pre-existing disease waiting period (2–4 years): Diseases declared at the time of buying the policy are covered only after this period ends.

- •Specific disease waiting period (1–2 years): Conditions like hernia, cataracts, joint replacement, and maternity are often excluded for the first 1–2 years.

How to avoid it:

- •Read your policy document thoroughly — especially the exclusions and waiting period clauses.

- •Plan elective procedures only after the relevant waiting period has lapsed.

- •Ask your insurer in writing whether your planned treatment is covered before admission.

Reason 3: Claim Filed for Excluded Treatments

What happens: Every health insurance policy has a list of permanent exclusions — treatments and conditions that are never covered, regardless of waiting period.

Common permanent exclusions in Indian health policies include:

- •Cosmetic surgery or aesthetic procedures

- •Dental treatments (unless due to an accident)

- •Weight loss or bariatric surgery (in many policies)

- •Fertility treatments, IVF, and assisted reproduction

- •Self-inflicted injuries or substance abuse complications

- •Experimental or unproven medical treatments

How to avoid it:

- •Request and carefully read the exclusions list of your policy before hospitalisation.

- •If unsure whether your procedure is covered, call your insurer's helpline and get written confirmation.

Reason 4: Incorrect or Incomplete Documentation

What happens: Insurance companies require a precise set of documents to process any claim — and even a small error or a single missing document can result in an outright rejection or long delays.

Documents commonly missing or incorrect:

- •Discharge summary not matching the diagnosis code (ICD-10) on the claim form

- •Missing original bills, pharmacy receipts, or investigation reports

- •Doctor's prescription not mentioning the diagnosis clearly

- •Mismatch between the patient's name on the insurance card and the hospital records

- •Unsigned claim forms or incomplete policy details

How to avoid it:

- •At Jigyasa Hospital, our dedicated insurance desk helps patients compile complete documentation from day one of admission.

- •Cross-check every document before submission — name, date of birth, policy number, and diagnosis must match exactly.

- •Always take 2 sets of all original documents and keep photocopies.

Reason 5: Hospitalisation for Less Than 24 Hours

What happens: Most standard health insurance policies cover only hospitalisation lasting a minimum of 24 hours. Shorter stays are often rejected.

Common daycare procedures that patients assume are covered — but aren't under standard policies:

- •Minor eye procedures (other than cataract)

- •Chemotherapy and dialysis (these are actually covered as daycare under most plans — but patients often don't know this)

- •Certain endoscopy or biopsy procedures

How to avoid it:

- •Check whether your policy includes a daycare treatment list — many modern policies now cover 500+ daycare procedures.

- •If your procedure is on the daycare list, make sure the hospital bills it under the correct procedure code.

- •Ask your treating doctor to document medical necessity clearly in the case files.

Reason 6: Lapsed Policy or Delayed Premium Payment

What happens: If your health insurance policy has lapsed — even by a few days — any hospitalisation during that gap will not be covered. Insurers have zero flexibility on this.

Why this happens more than you'd think:

- •Auto-renewal failure due to outdated bank details or insufficient account balance

- •Forgetting renewal amid a health crisis (ironically, when you need it most)

- •Switching jobs and losing group health cover without buying an individual policy in time

How to avoid it:

- •Set a calendar reminder 30 days before your policy renewal date.

- •Enable auto-debit for premium payments and keep your bank account adequately funded.

- •If you are between jobs, buy a short-term or individual policy immediately — never stay uninsured.

- •Use the grace period (15–30 days after expiry) wisely — but note that claims during the grace period may still be denied by some insurers.

Reason 7: Treatment at a Non-Empanelled or Unapproved Hospital

What happens: For cashless claims, your insurer will only process the claim if your hospital is on their approved network list. Treatment at a non-network hospital forces you to go through the reimbursement route — and may reduce your claim amount significantly.

For Ayushman Bharat (PM-JAY) beneficiaries: Treatment is only valid at government-empanelled hospitals. Claims submitted for treatment at non-empanelled facilities are automatically rejected.

How to avoid it:

- •Before admission — especially for planned procedures — always verify that your hospital is on your insurer's network.

- •Jigyasa Hospital, Moradabad is empanelled under Ayushman Bharat (PM-JAY) and is a registered partner with multiple major insurance providers — making the claim process smoother for our patients.

- •Always carry your insurance card and Ayushman card when visiting a hospital.

What To Do If Your Claim Gets Rejected

- •Step 1: Request the rejection letter with the specific reason in writing from your insurer.

- •Step 2: Cross-check the reason against your policy document — sometimes rejections are errors.

- •Step 3: File a grievance with your insurance company's internal ombudsman within 30 days.

- •Step 4: If unresolved, escalate to the Insurance Ombudsman (free, government-backed) or the IRDAI helpline: 155255.

- •Step 5: Consult the patient services team at your hospital — they often have experience resolving disputes with specific insurers.

How Jigyasa Hospital Helps You Get Your Claim Approved

- •Our dedicated Insurance and TPA Desk is operational 7 days a week to assist patients with pre-authorisation, documentation, and claim follow-ups.

- •We are empanelled with Ayushman Bharat PM-JAY, CGHS, and major private insurers — enabling seamless cashless treatment for eligible patients.

- •Our team proactively coordinates with your insurer from the moment of admission to ensure your discharge and billing documentation is claim-ready.

- •We offer transparent pricing — no surprise bills that could disqualify your claim on technical grounds.

Insurance Helpdesk: 7900903333

Address: Near Miglani Cinema, Rampur Road, Moradabad – 244001

Website: jigyasahospital.com

Cashless Insurance | Ayushman Bharat PM-JAY | TPA Assistance | Transparent Billing | 7-Day Insurance Desk

Key Takeaways

- •Health insurance claim rejections in India are most commonly caused by non-disclosure, waiting periods, exclusions, poor documentation, short hospitalisations, lapsed policies, and non-empanelled hospitals.

- •Almost every rejection reason is preventable with awareness and preparation before you are admitted.

- •Read your policy document thoroughly — especially the fine print on exclusions and waiting periods.

- •Always choose a hospital empanelled with your insurer for smooth cashless processing.

- •Jigyasa Hospital's patient services team is here to guide you through every step of the insurance and claim process — so you can focus entirely on recovery.

Frequently Asked Questions

What is the most common reason health insurance claims are rejected in India?

Non-disclosure of pre-existing conditions is the single most common reason for claim rejection in India. If a condition was not declared at the time of policy purchase, insurers can legally deny any related claim — even years after the policy was issued.

Can my claim be rejected if I was hospitalised for less than 24 hours?

Yes, under most standard policies, hospitalisation must last at least 24 hours to qualify for a claim. However, many modern policies include a daycare treatment list covering procedures that do not require overnight admission. Check your policy document or ask your insurer before undergoing a short-stay procedure.

What should I do if my cashless claim is denied at the hospital?

Request the denial reason in writing from the insurer's TPA desk at the hospital. Cross-check it against your policy. If it appears to be an error or a documentation issue, the hospital's insurance desk can often help resolve it before discharge. If denied after discharge, file a formal grievance with your insurer within 30 days.

Is Jigyasa Hospital empanelled under Ayushman Bharat PM-JAY?

Yes. Jigyasa Hospital, Moradabad is empanelled under Ayushman Bharat PM-JAY and is a registered partner with multiple major private insurers. Eligible patients can avail cashless treatment directly. Carry your Ayushman card and insurance card at the time of admission.

Can I appeal a rejected health insurance claim?

Yes. First, file a written grievance with your insurer's internal grievance cell. If unresolved within 30 days, escalate to the Insurance Ombudsman — a free, government-backed dispute resolution body. You can also contact IRDAI directly on their helpline 155255 or at www.irdai.gov.in.

What documents are required for a health insurance claim in India?

Typically required documents include the original discharge summary, all hospital bills and pharmacy receipts, investigation reports, doctor's prescription mentioning the diagnosis, duly filled and signed claim form, policy card, and valid photo ID. Missing or mismatched documents are a leading cause of delays and rejections.

Will my claim be covered if my policy has just lapsed?

No. Any hospitalisation during a lapsed policy period — including most grace periods — is not covered. Some insurers may allow grace period claims, but this varies by insurer and policy type. Always ensure your policy is active and renewed before any planned procedure.

Are cosmetic surgeries covered under health insurance in India?

No. Cosmetic and aesthetic procedures are permanent exclusions under virtually all Indian health insurance policies — unless the procedure is medically necessary as a direct result of an accident or reconstructive requirement.

How long does it take for a health insurance claim to be processed?

For cashless claims, insurers must respond to pre-authorisation requests within 1 hour for emergencies and within 3 hours for planned admissions. Reimbursement claims typically take 15–30 working days after submission of complete documents. Delays are most often caused by incomplete documentation.

Does Jigyasa Hospital assist with insurance documentation and claims?

Yes. Jigyasa Hospital has a dedicated Insurance and TPA Desk operational 7 days a week. Our team assists with pre-authorisation, documentation compilation, and claim follow-ups from the day of admission through to discharge — so patients and families can focus on recovery rather than paperwork.

Related Articles

Heart Attack Warning Signs You Must Never Ignore

Recognizing heart attack symptoms early can save your life. Learn the critical warning signs from Dr. Amit Kumar Singh, Senior Interventional Cardiologist at Jigyasa Hospital, Moradabad. Call 7900903333.

5 Early Morning Habits That Prevent Diabetes Naturally

Discover 5 powerful morning habits that naturally prevent diabetes. Expert advice from Dr. C.P. Singh, Senior Consultant Physician at Jigyasa Hospital, Moradabad. Call 7900903333.

Why Summers in UP Are Dangerous for Your Kidneys

UP summers can silently damage your kidneys. Jigyasa Hospital Moradabad explains the hidden risks, warning signs, and how to protect your kidneys this season. Call 7900903333.